What is Anti Money Laundering?

Money laundering is when criminals integrate their illegally obtained cash into the financial system, so it looks like it was earned legitimately. Anti-money laundering constitutes the laws, regulations, and procedures designed to prevent money laundering.

We can help you stay compliant

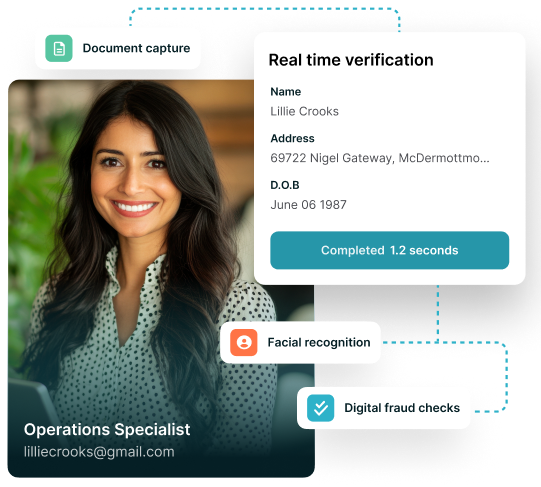

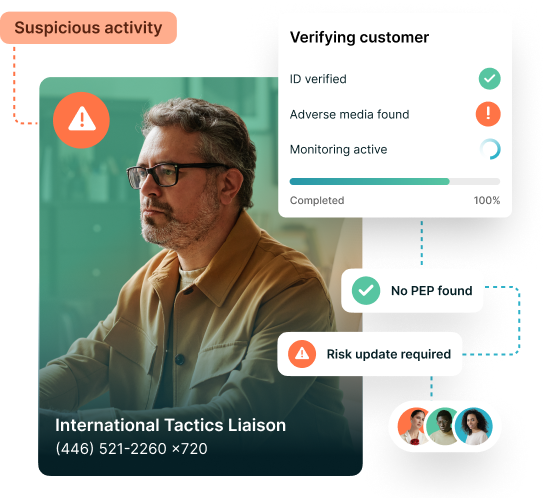

The SmartSearch platform is a one-stop-shop for all your AML requirements. Our user-friendly system means team members at any level can perform identification verification KYC checks easily and effectively and, thanks to the fully integrated app, can run checks remotely too. The details of each customer you identify, verify and screen will be automatically saved into the system to ensure watertight record-keeping, meaning you only need one system for all your CIP and Customer due diligence need. What’s more, the platform is constantly updated and improved to ensure you never have to upgrade to remain compliant.