AML Checks Made Easy

All in all, SmartSearch is the go-to AML compliance platform built to easily verify clients that are based not only in the UK but on a global scale. Our platform has the following features that make anti-money laundering checks far easier:

- A convenient central hub for use in managing all aspects of KYC and due diligence

- Checking mechanisms that are more time and cost-effective than manual checking

- Access to more data and information in comparison to the competition

- Access to international data, allowing you to easily onboard overseas customers

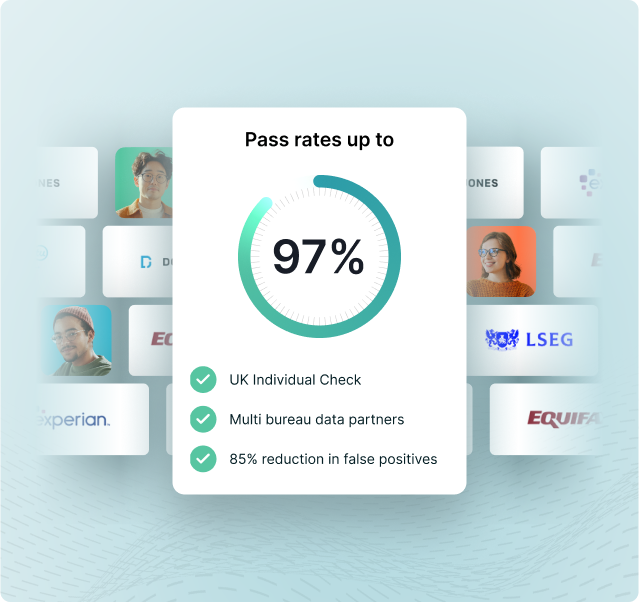

- Industry-leading pass rate of up to 97%

What Are Anti-Money Laundering Checks?

Anti-money laundering checks — or ‘AML checks’, as they are often casually called — are, to a large extent, self-explanatory. They are indeed aimed at preventing money laundering. A business will often use AML checks to identify and verify prospective customers.

For the purpose of judging a customer’s money laundering risk and complying with AML regulations, businesses could check information about the following subjects:

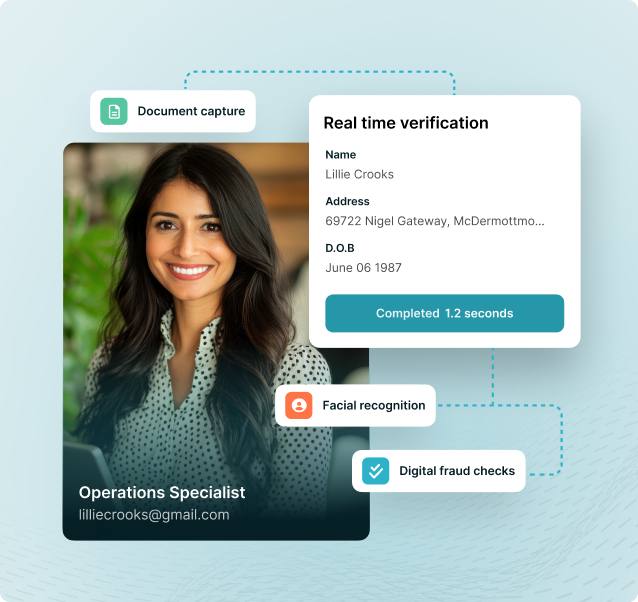

- The customer’s name, residential address, and date of birth

- The corporate relationship’s purpose and intended nature

- The customer’s business or employment

- The source or origin of the customer’s funds

Explore our exclusive AML Software

We have a number of exclusive services and softwares to help make the AML process streamlined and functional. See how our SmartSearch technology can help your AML compliance:

Want To See It In Action?

Let one of our highly trained sales team members demonstrate the multi-award-winning SmartSearch AML product.

/SmartSearch_OfficeLifestyle_Feb25_115%201.jpg?width=950&height=950&name=SmartSearch_OfficeLifestyle_Feb25_115%201.jpg)

What Does This Mean For Your Company?

The latest ECCTA bill is being brought in to improve company transparency in aid of better combating financial crime. As a result, businesses may experience wide-ranging implications, with increased due diligence being the most significant change. Under the forthcoming legislation:

- From spring 2025, all directors and PSCs will have to verify their identity when setting up a company.

- Existing businesses will have a 12-month transition period wherein they’ll be expected to verify the identity of directors and PSCs when filing their new Confirmation Statement.

The Help You Need, Exactly When You Need It

Whether you’re a small business just getting to grips with AML regulations or a large corporation with plenty of experience in compliance, SmartSearch can help you to comply with regulations, fight financial crime and grow your business with confidence.

-

Case Studies

Explore case studies of how our clients have used our services to streamline their businesses and excel.

-

Blogs

Discover our latest blog posts for expert tips, features, industry trends and more.

-

Effortless Verification of Customers

At SmartSearch, our AML screening software makes it effortless to carry out your mandatory AML checks. Offering a variety of solutions that allow you to conduct comprehensive anti-money laundering checks to a high standard, we can help you perform your due diligence today and stay compliant going forward. Perform a complete anti-money laundering search that allows you to:

/SmartSearch_OfficeLifestyle_Feb25_063.jpg?width=855&height=855&name=SmartSearch_OfficeLifestyle_Feb25_063.jpg)

There’s a Reason Over 7,000 Clients Put Their Trust in Us