Customer Due Diligence procedures are a core element of anti-money laundering regulations

See it in action

Let one of our highly-trained sales team demonstrate the multi-award winning SmartSearch AML product.

/SmartSearch_OfficeLifestyle_Feb25_115%201.jpg?width=950&height=950&name=SmartSearch_OfficeLifestyle_Feb25_115%201.jpg)

Understanding the different levels of Customer Due Diligence

.png?width=855&height=855&name=UK%20Individual%20(2).png)

The help you need, when you need it

Whether you’re a small business just getting to grips with AML regulations or a large corporation with plenty of experience in compliance, SmartSearch can help you to comply with regulations, fight financial crime and grow your business with confidence.

-

Resource library

Explore our resource library for expert guides and tools to support your compliance processes.

-

Blogs

Discover our latest blog posts for expert tips, features, industry trends and more.

-

There’s a reason over 7,000 clients put their trust in us

Serving professional AML regulated industries

Trusted by over 7,000 regulated businesses, SmartSearch's next-generation technology is the UK's leading solution for AML and risk management.

What is the difference between customer due diligence (CDD) and know your customer (KYC) processes?

While KYC—‘Know your Customer’—is all about those initial checks before starting any business relationship (think of it as the screening process, like checking the guest list before the party starts), CDD goes a step further. Customer Due Diligence doesn’t just stop at onboarding; it includes continually assessing risk and monitoring the ongoing activities of your customers for anything unusual or suspicious.

So, in a nutshell:

- KYC covers those essential first steps to confirm a customer's identity.

- CDD builds on that foundation with regular reviews and monitoring to catch changes or risks as they arise.

Both are designed to keep businesses compliant and help spot financial crime—but CDD keeps an eye on things long after the welcome mat has been rolled out.

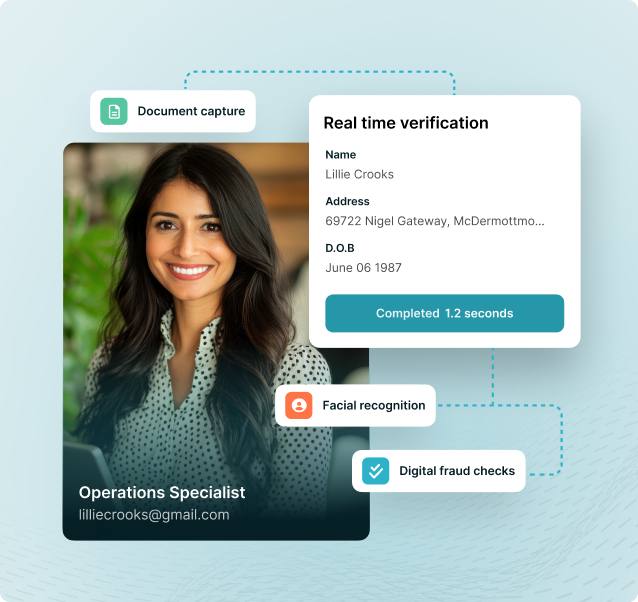

Streamlining Customer Due Diligence with SmartSearch

With SmartSearch, your Customer Due Diligence (CDD) process becomes a streamlined, efficient experience. Our advanced platform automates the identification and verification of customer information, ensuring compliance with AML regulations. By accessing a wide range of reliable data sources, including passports, driving licenses, and utility bills, SmartSearch helps you quickly and accurately verify customer identities, reducing risk and saving valuable time.

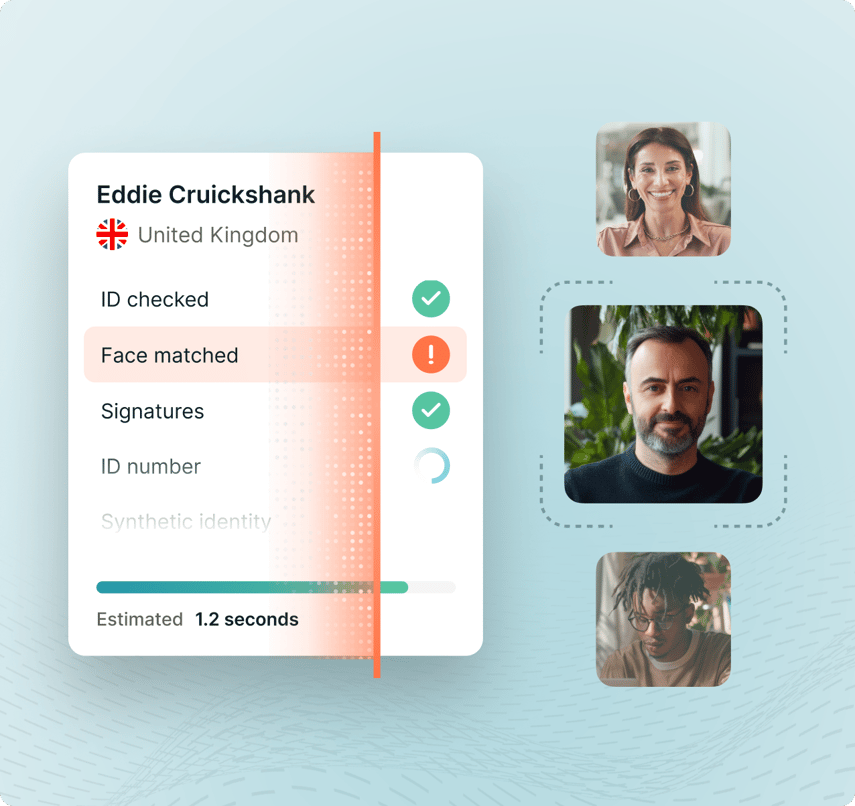

The Power of Automated Simplicity

Automating the majority of initial CDD checks not only accelerates the process but also helps pinpoint high-risk cases that require further investigation. This approach saves you time, reduces operational costs, and minimizes the risk of human error—allowing your teams to focus on more value-added tasks.

For low-risk customers, SmartSearch slashes processing times from hours to near real-time, enabling you to meet client expectations and engage them before competitors can. The result: better conversion rates, smoother onboarding, and a seamless journey for both your business and your customers.