Driving innovation with trusted solutions for Investment Firms

We are committed to helping our clients achieve their goals through secure and efficient solutions

-

Verify your customer

Identifying and verifying customers and taking all the steps you need to remain compliant takes just seconds with our platform. Use our platform to complete your KYC AML checks within your financial institution.

-

Customer onboarding

Streamline customer onboarding and enhance your client experience with our award-winning platform that negates time-consuming traditional verification methods and minimizes cost and resource for your business.

-

/SmartSearch_OfficeLifestyle_Feb25_004.jpg?width=462&height=293&name=SmartSearch_OfficeLifestyle_Feb25_004.jpg)

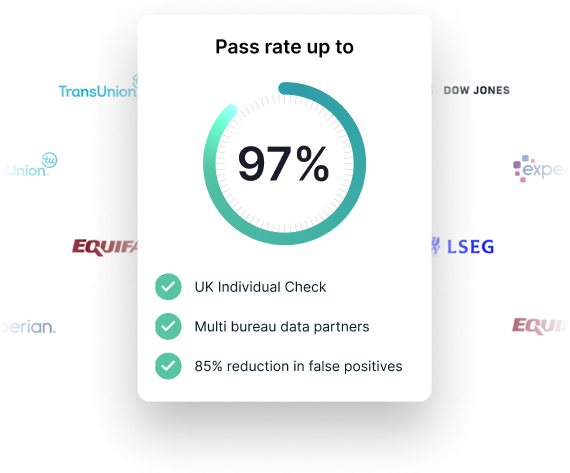

Do your due diligence

Automate the bulk of your enhanced due diligence using our unique system to automatically discount any false positives, ensuring you remain compliant with minimal effort. A game-changing feature for AML in finance.

-

Monitor your clients

Powered by Dow Jones, our ongoing monitoring feature reviews PEP and Sanction watchlists globally, alerting you to any status changes and keeping you compliant at all times.

-

Prevent fraud

We offer a wide range of anti-fraud products and services that can be tailored to your firm's specific requirements.

-

Be audit ready

Get prepared for audits by using our batch upload feature, ongoing monitoring and automated audit notes, you can be confident that your processes are watertight, and your business will always be audit-ready.

Integrate SmartSearch’s capabilities into your own system

We simplify the KYC process for AML in finance, verifying your clients in both the UK and overseas, so you can get on with what you do best. Get a personalised quote for your financial institution today, and find out how much you could save.

SmartSearch is able to integrate our services with your existing software, so you can run AML checks using information from your own system.

.png?width=400&height=70&name=Advanced%20(2).png)

Advanced delivers robust, cutting-edge solutions for optimised business operations.

Alto Software offers a comprehensive cloud-based property management solution for estate agents.

Wealth Dynamix provides CLM solutions for wealth management.

Salesforce streamlines sales, marketing, and customer service with its CRM tools.

.png?width=400&height=70&name=worxinfo%20(2).png)

Worxinfo creates efficient, tailored data systems for organisations.

Our AML and compliance solution is trusted by over 2,000 financial firms

.png?width=204&height=65&name=coop%20(2).png)

.png?width=204&height=65&name=Greystone%20(2).png)

We offer cutting-edge technology that instils trust and build confidence for finance firms

There are a number of steps that a UK financial services provider should take to ensure compliance with the Money Laundering Regulations. These include, but are not necessarily limited to:

- Ensuring the firm has written policies, controls, and procedures to mitigate the AML fraud risk.

- Making sure those policies, controls, and procedures cover risk management practices, internal controls, customer due diligence, reliance and record keeping, and the monitoring and management of compliance.

- Communicating the policies, controls, and procedures to staff.

- Providing up-to-date staff training on the organisation’s policies and procedures, and how to report suspicious activity.

Additional measures to ensure compliance for your finance firm

- Ensuring the firm is registered with the Information Commissioner’s Office under the Data Protection legislation

- Carrying out a risk assessment on itself in relation to money laundering or terrorist financing risks

- Putting procedures in place to check a client’s identity and business activities, in order to mitigate the risk of money laundering activity

- Carrying out enhanced due diligence on higher-risk customers

- Ensuring the firm has reviewed and updated its AML policies, procedures, and controls in the last 12 months

- Keeping AML records for at least five years after a business relationship with a client ends

How our resources can support you

-

Resource library

Explore our resource library for expert guides and tools to support your compliance processes.

-

Blogs

Discover our latest blog posts for expert tips, features, industry trends and more.

-